PARTNERS

Boost Your Solar Sales with Midas Wealth – Higher Commissions, Happier Homeowners

Partner with us to unlock up to 50%-90%+ returns for customers and maximize your earnings with ease

Challenges in Solar

Struggling with delayed commissions, high cancellation rates, or customers who “don’t qualify” because they have no tax liability? You’re not alone. Reps everywhere are running into the same issues — confused homeowners, stalled installs, and deals slipping through the cracks.

Midas Wealth Solution

Midas Wealth offers a game-changing tax product that commercializes solar systems, unlocking 50-90%+ returns for homeowners, including commissions and charges, while reducing overall costs. It’s the only add-on that makes solar deals cheaper, easier to sell, and backed by Kevin O’Leary from Shark Tank.

And for homeowners without tax liability?

We pay them cash for their credits, turning an unused tax benefit into real upfront money that reduces financing, lowers payments, and makes solar more accessible than ever.

Try it on one of your Deals

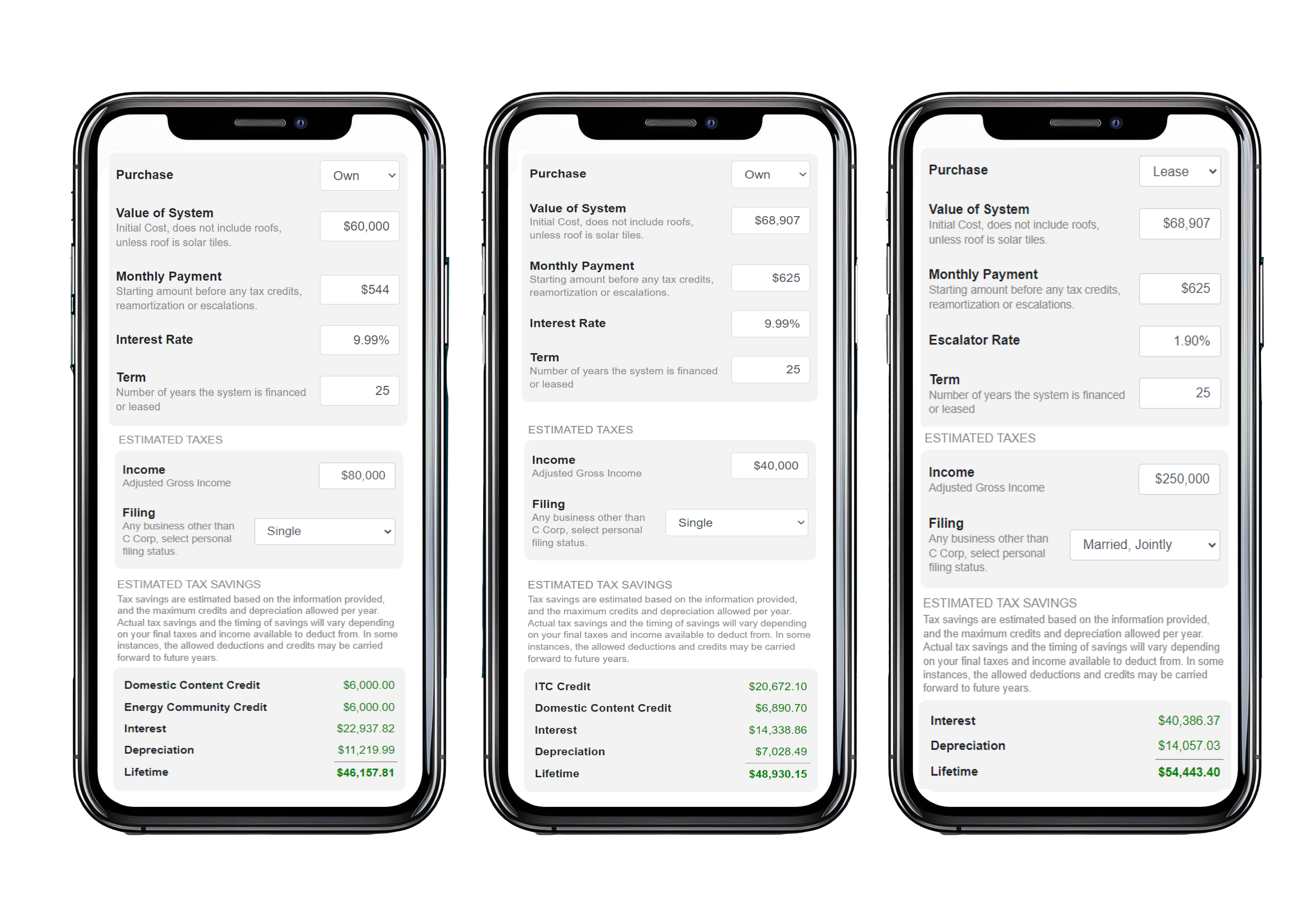

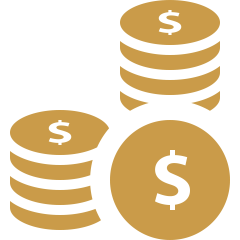

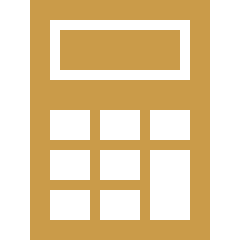

Calculate one of your deals

Benefits For Partners

Increased Commissions

Earn more without hurting homeowners, with payouts in 2 weeks vs. 6-8 months for traditional solar deals.

Easier Sales

Our calculators (tax liability, incentives) help qualify leads, simplifying pitches and building trust.

Better Expectations

Set clear homeowner expectations, reducing backlash from unmet tax credit promises, unlike last year’s industry issue

Additional Revenue

Become a Referral Partner for overrides (e.g., $50-$100 per deal) when introducing other companies, scaling quickly with high-volume partners (200-1,000 deals/month).

Credit Transfers

Revolutionize sales with our credit transfer system, offering homeowners checks post-install boosting sales.

Benefits For Homeowners

More back on Investment

Homeowners get 50-90% back on solar, accessing commercial benefits like energy community grants and rebates, reducing net costs and increasing satisfaction.

Fulfillment of their ITC

80% of solar homeowners haven’t claimed traditional ITCs due to confusion; Midas helps, improving industry trust and reducing cancellations to 5% from 20%.

What is solar commercialization, and why does it matter now?

Solar commercialization is the legal process of restructuring your solar system as a for-profit business (typically an LLC) rather than a personal residential asset. This allows you to access commercial tax benefits—including the Section 48E investment tax credit (up to 30% or more), MACRS accelerated depreciation, and business expense deductions, rather than just the standard residential tax credit.

How is this different from just claiming depreciation on my residential

system?

It's completely different. We don't advise claiming depreciation while keeping the residential credit. We help you properly convert to commercial treatment and claim the commercial Section 48E credit instead.

What specific tax benefits come from commercialization?

The 30% Investment Tax Credit (Section 48/48E), 5-year accelerated depreciation (MACRS), and business expense deductions (Section 162). Plus potential 10% bonus adders for domestic content or energy community locations. Combined, these can return 50-70% Sometimes more of your system cost depending on customer tax bracket.

Is this legitimate under IRS rules?

Yes, when structured correctly. Our approach is backed by a comprehensive legal opinion from Nelson Mullins Riley & Scarborough LLP, one of the nation's leading law firms with over 125 years of regulatory and business law expertise. They would defend this strategy in court.

Who can do this? Is commercialization right for me?

Anyone installing solar who has tax liability to offset and demonstrates genuine business intent (such as selling power to the utility or offsetting consumption costs) can potentially benefit. It's particularly valuable for

those with significant taxable income.

What are the biggest risks I should know about?

The audit risk is extremely low, IRS audit selection systems are notoriously outdated, and small partnership returns attached to individual 1040s are not audit triggers. The estimated chance of this specific activity triggering an audit is less than one-hundredth of one percent. However, low audit risk is not our justification, our approach is defensible because it's legally sound. If a client were audited for unrelated reasons and this came up, the documentation and legal framework we provide is designed to survive scrutiny. We've consulted with IRS representatives directly, and they've confirmed that properly established businesses reporting business income are treated appropriately. Nelson Mullins would defend our approach in court if challenged.

What are FEOC and "material assistance" rules?

FEOC refers to "Foreign Entity of Concern" essentially prohibited foreign entities (such as those 25% or more foreign-owned or controlled by certain countries). Starting in 2026, credits are not available for systems with FEOC involvement. "Material assistance" rules disqualify credits if too much of the system cost (40% or more, rising over time) comes from FEOC sources. Given the prevalence of Chinese components in solar manufacturing, supply chain verification is essential. Midas helps ensure compliance with these requirements.

What if I don't have enough tax liability to use the credits?

This opens up your market dramatically. Homeowners with no tax liability, who would previously have received zero benefit from tax credits, can now receive an actual cash check. On a $100,000 system, that's $25,000. This makes solar viable for an entirely new demographic.

How does Midas sell the tax credits? Is there demand?

There is far more demand for tax credits than supply. Fortune 500 companies have roughly $400 billion in annual tax liability, while total available tax credits are estimated at $40-50 billion. Midas holds all equity in tax equity transfers and maintains direct relationships with tax equity buyers. We work with experienced capital markets professionals who broker tax equity investments to institutional buyers. The credits we offer are priced competitively, making them highly attractive to investors.

How does Fund II work for investors?

Investors select from multiple investment packages with varying return profiles and timeframes: Package A offers approximately 28% IRR over 12 months, Package B offers approximately 35% IRR over 24 months, and Package C offers approximately 41% IRR over 36 months. The structure monetizes credits through equity participation and K-1 allocations. Midas manages all investor relationships and fund operations.

Where is the actual business income coming from?

The income comes from two sources: (1) electricity sold back to the utility through net metering arrangements, and (2) the economic value of electricity consumed by the home, which reduces utility bills. Both represent taxable barter income under well-established tax law, just like a farmer who either sells or

consumes their own crops. If a farmer eats their own cow instead of selling it, that's still income. When your home uses electricity you generated instead of paying the utility, you've increased your net worth, that's income and demonstrates a clear profit motive.

How does Midas handle economic substance requirements under

Section 7701(o)?

Our structure follows the Nelson Mullins legal opinion, which is designed for real business operations with genuine profit motive. The LLC is structured with proper documentation, separate bank accounts, ongoing

management activities, and arm's-length transactions. If needed for additional protection, Form 8275 disclosure can be filed with the return. The focus is on establishing and documenting reasonable basis for all positions taken.

Won't the IRS classify this as a hobby and disallow the deductions?

No. Solar energy generation does not have the characteristics of a hobby. There's no personal pleasure element (unlike a horse farm or yacht), clear profit motive exists (reduced bills = increased net worth), and the activity is conducted in a businesslike manner with proper documentation.

How do I report commercialized solar on my taxes?

Our exclusive tax partner, Paramount Tax and Accounting, handles all tax reporting. Depending on your structure, this typically involves Schedule C (for single-member LLCs) or Form 1065 (for partnerships), plus Form 3468 for the Investment Tax Credit.

What documentation do I need to maintain?

Midas provides all the legal documentation: LLC formation papers, Operating Agreement, Contribution Agreement, and related transaction documents. You'll also need to maintain energy production records, utility statements, and invoices which Paramount Tax and Accounting uses for tax reporting. For bonus

credits like domestic content, supplier certifications may be required, which Midas helps coordinate.

Are there state-specific considerations?

Yes, state incentives like rebates and additional credits vary by location. Midas operates across multiple states and ensures compliance with state-specific requirements. Paramount Tax and Accounting handles state tax filing requirements. The federal commercialization framework is consistent nationwide, but state benefits can add significant additional value depending on where you live.

My CPA says this won't work. What should I do?

Offer to provide the CPA with our Letter to Accountants document, which explains the legal foundation in professional terms. Emphasize that Midas is not an accounting firm—we handle LLC setup and equity structuring, while Paramount Tax and Accounting handles all tax work. Our approach is backed by Nelson Mullins and has been reviewed by tax litigation professionals with experience defeating IRS claims on these very issues.

Should I have my own CPA review this before proceeding?

Absolutely. We encourage you to consult with your own tax professional. We're happy to provide them with information about our approach. Every taxpayer's situation is unique, and your CPA knows your complete financial picture. They're welcome to coordinate with Paramount Tax and Accounting if they have technical questions about the tax implementation.

How does Midas reduce my risks?

Midas provides turnkey LLC formation with proper legal structure, comprehensive documentation backed by Nelson Mullins legal analysis, and coordination with Paramount Tax and Accounting for compliant tax filing. For Full Transfer clients, Midas holds all equity and manages investor relationships, taking on transaction risk. Our Fund II structure offers multiple investment packages designed to monetize credits safely while protecting all parties.

What if my tax situation changes after I commercialize?

Unused credits can be carried forward for up to 20 years. If you have more credits than you can use, the Full Transfer option allows Midas to sell the tax benefits to investors on your behalf. Paramount Tax and Accounting can help plan for changing circumstances and optimize credit utilization across multiple tax years.

What happens if I sell my house? Will I face recapture?

Our structure separates ownership of the solar equipment from ownership of the real property. The LLC owns the solar system through operating agreements and retains that ownership regardless of what happens to the house. If you sell your home, you have options: you could keep the property as a rental (no recapture issue at all), transfer the LLC interest to the new homeowner in a separate transaction (potentially triggering recapture, but negotiated as part of the sale price), or maintain the LLC's ownership arrangement with the new property owner. Additionally, the typical holding period for homes often exceeds the five-year recapture period due to capital gains exclusion rules, most homeowners hold properties long enough that recapture is no longer a concern.

Can I convert a system I already claimed the 25D credit on?

Yes. Amended returns can be filed within three tax seasons to properly restructure your tax treatment. The IRS doesn't object to taxpayers reporting additional business income, in fact, our commercialization approach results in reported gross income that would not otherwise appear on the return. Paramount Tax and Accounting handles the amended return preparation, and Midas establishes the proper business structure going forward.

How do bonus credits work, like domestic content?

The domestic content bonus adds 10% to your ITC for using U.S.-manufactured components meeting threshold requirements (45% in 2025, rising to 55% later). Safe harbor certifications are available to verify compliance. Energy community bonuses (another 10%) apply to approximately 30% of installations based on location. Midas helps identify which bonuses you may qualify for, and Paramount Tax and Accounting ensures proper certification and claiming.

What percentage of clients qualify for bonus credits?

Approximately 30% of clients qualify for energy community bonuses based on their location. Domestic content qualification is less common currently due to supply chain realities, but this is improving as more U.S. manufacturing comes online, particularly with newer products from manufacturers like Tesla. Virtually all

clients who proceed complete the LLC formation successfully; only a small percentage decline or are unable to proceed for other reasons.

What does Midas charge for these services?

Setup fees typically range from $3-4,000 depending on the complexity of your situation. The value proposition is significant, clients typically receive tax benefits worth many multiples of the setup cost. Even clients who only qualify for the base 30% ITC (without bonuses or depreciation) generally find the

offset value exceeds the cost. Refund rates for disqualification (such as inability to form an LLC) are low, and we can often shift to alternative structures.

Ready to transform your solar business?

Fill out the form below to join our Partner Program and schedule a demo. Let’s grow together!

© Copyright 2026. Midas Wealth. All Rights Reserved.